Basics of Shale Gas

It was long known that shales may contain significant amounts of oil or natural gas. But only technology advances in directional drilling and hydraulic fracturing made it possible to extract these ressources economically. The Barnett Shale in Texas, U.S. was the first shale gas play to be exploited at large-scale, with intensive drilling starting in the late 1990s.

What is shale gas?

Shale Gas is natural gas that is present in shale rocks. Throughout the world, different types of sedimentary rock contain natural gas deposits, for example sandstones, limestones or shales. Sandstone rocks often have high permeability, which means that the tiny pores within the rock are well connected and gas can flow easily through the rock. In contrast, shale rocks usually have very low permeability, making gas production more complex and costly.

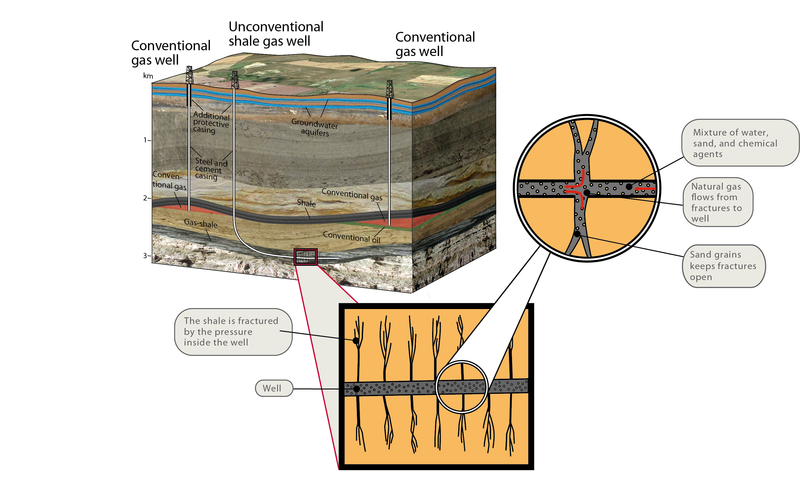

Fig. 1: Conventional gas wells, shale gas well, and the process of hydraulic fracturing.

Fig. 1: Conventional gas wells, shale gas well, and the process of hydraulic fracturing.Shale gas is considered a so-called “unconventional gas”, together with “tight gas” from sandstones or limestones with low permeability and “coal bed methane” (CBM). While both conventional and unconventional deposits do host natural gas, it’s the more elaborate production methods that distinguish unconventional from conventional deposits; hydraulic fracturing (Fig. 1) is often applied to unconventional natural gas deposits. The distribution of different types of natural gas deposits varies around the world´s different regions, see Fig. 2.

Formation

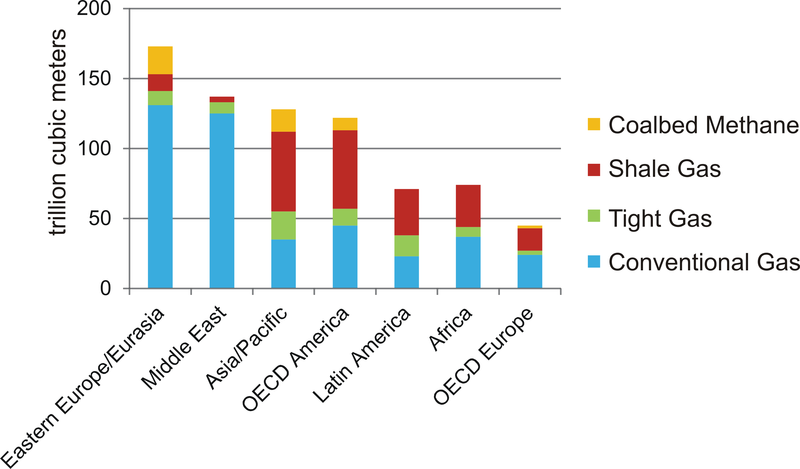

Fig. 2: Distribution of conventional and unconventional natural gas resources in the world´s regions (Data from: Golden Rules for a Golden Age of Gas, IEA, 2012).

Fig. 2: Distribution of conventional and unconventional natural gas resources in the world´s regions (Data from: Golden Rules for a Golden Age of Gas, IEA, 2012).Like oil and coal, natural gas in shales has, essentially, formed from the remains of plants, animals, and micro-organisms that lived millions of years ago. Though there are different theories on the origins of fossil fuels, the most widely accepted is that they are formed when organic matter (such as the remains of a plant or animal) is buried, compressed and heated in the earth´s crust for long time. In the case of natural gas, this is referred to as thermogenic methane generation.

Though the basic principles of shale gas formation are fairly well understood, generation of the gas within individual shales may differ significantly. Better knowledge is needed e.g. on basin modeling, petrophysical characterization, or gas flow in shales for an improved understanding of unconventional reservoirs.

For European gas shales this research is conducted within GASH, the first European interdisciplinary shale gas research initiative. GASH integrates available knowledge on European shales and conducts research projects in order to predict shale gas formation and occurrence in time and space.

Where is it found?

Shales are present worldwide in the sedimentary sequence. Large sedimentary basins, where sediments accumulated over millions of years, are favorable places to find large extent shale deposits of sufficient thickness. Certainly not all shales contain reasonable quantities of natural gas. Geologic modeling can lead exploration geologists to promising locations, and the subsequent investigation of drilled rock samples will eventually give information on the gas content of the shales.

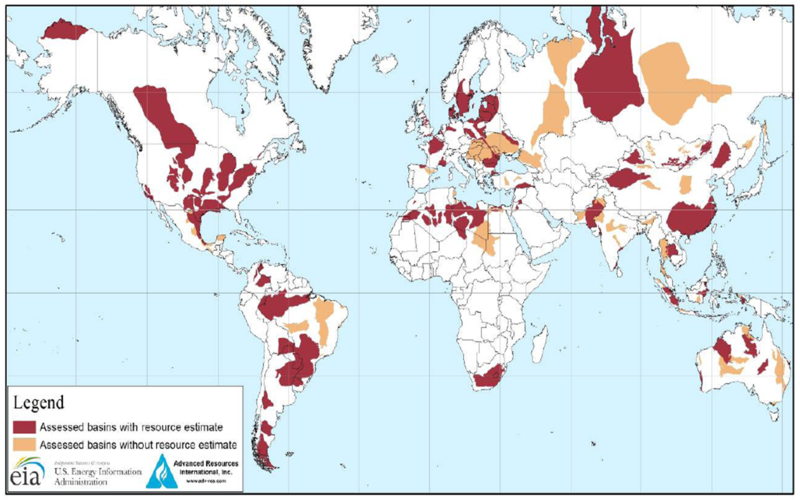

Since large-scale shale gas production is ongoing only in North America, information on the location of gas shales worldwide is rather incomplete. The 2013 U.S. EIA report "Technically Recoverable Shale Oil and Shale Gas Resources: An Assessment of 137 Shale Formations in 41 Countries Outside the United States" summarized information on 95 shale basins in 41 countries (Fig. 1), including brief descriptions of the geology, reservoir properties, resources and activities in individual basins.

Fig. 1: Map of major shale gas basins in 41 countries (EIA, 2013).

Fig. 1: Map of major shale gas basins in 41 countries (EIA, 2013).

North America

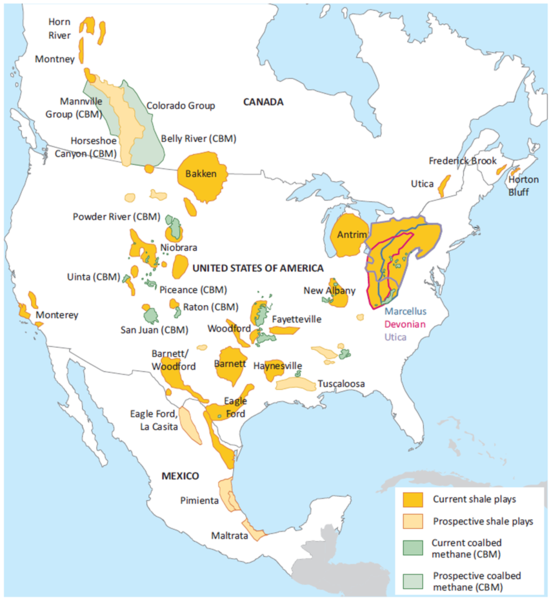

The large shale gas formations of North America are shown in Fig. 2. Many of the shales have been proven to contain natural gas and are already being exploited. Large-scale shale gas production started in the U.S. in the Barnett shale, Texas, in the late 1990s.

Fig. 2: Natural gas resources of North America (IEA, 2012).

Fig. 2: Natural gas resources of North America (IEA, 2012).

Europe

Whether the large shale deposits in Europe (Figs. 3-5) are promising for large-scale shale gas production is in most cases yet unknown. A few prospective wells have been drilled, and scientific investigations are now being carried out to find and compile data on where to locate the shales and also how they formed.

A prominent effort in this respect is the project "Gas Shales in Europe" (GASH). It is the first European interdisciplinary shale gas research initiative. Coordinated by GFZ German Research Centre for Geosciences, GASH is developing a GIS-based European black shale database, and is conducting 12 research projects with a multinational expert task force drawn from research institutions, geological surveys, universities and consultants.

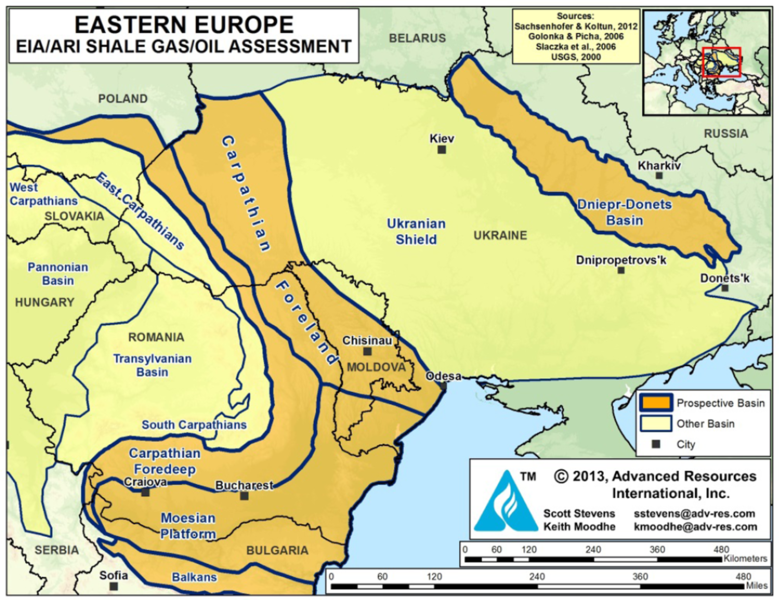

Fig. 3: Prospective shale gas basins of Eastern Europe (EIA, 2013).

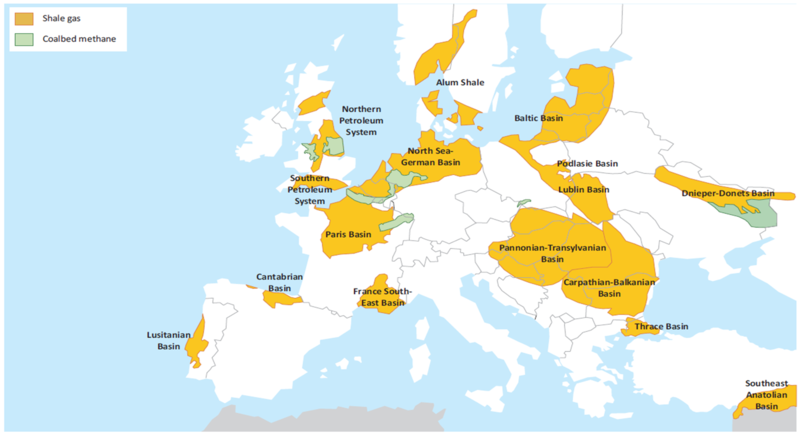

Fig. 3: Prospective shale gas basins of Eastern Europe (EIA, 2013). Fig. 4: Shale gas basins and coalbed methane of Western Europe (IEA, 2012).

Fig. 4: Shale gas basins and coalbed methane of Western Europe (IEA, 2012). Fig. 5: Assessed shale gas basins of Poland (EIA, 2013).

Fig. 5: Assessed shale gas basins of Poland (EIA, 2013).What are the benefits?

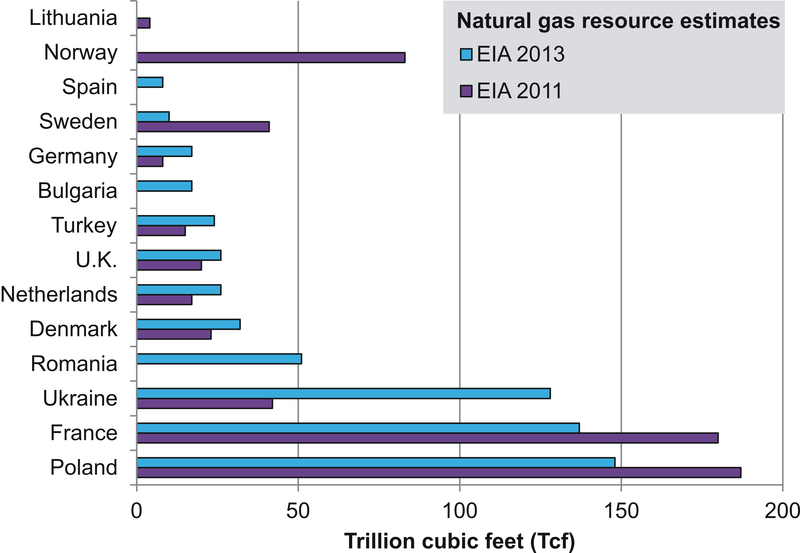

Fig. 1: Estimated technically recoverable shale resources for selected basins in some European countries (Data from U.S. EIA “World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States", 2011 and "Technically Recoverable Shale Oil and Shale Gas Resources: An Assessment of 137 Shale Formations in 41 Countries Outside the United States”, 2013).

Fig. 1: Estimated technically recoverable shale resources for selected basins in some European countries (Data from U.S. EIA “World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States", 2011 and "Technically Recoverable Shale Oil and Shale Gas Resources: An Assessment of 137 Shale Formations in 41 Countries Outside the United States”, 2013).Secure energy supplies

According to the U.S. Energy Information Administration (EIA) report, 2013, the United States possesses 567 trillion cubic feet (Tcf) of technically recoverable shale gas. At the 2012 rate of U.S. gas consumption, this represents enough supply for 22 years of use. In 2011, 34 % of all U.S. natural gas produced was shale gas, and this could rise to 50 % of U.S. total natural gas production in 2040, as projected in the EIA Annual Energy Outlook 2013.

Shale gas resource estimates for some European countries are shown in Fig. 1, indicating very large shale gas resources for some countries. Please note that updates of the data shown in Fig. 1 are available: Poland: 12-27 (possibly up to 67) Tcf (Polish National Geological Service; March, 2012); Germany: 11-71 Tcf technically recoverable resources (German Federal Institute for Geosciences and Natural Resources; January, 2016), U.K**: 822-2281 Tcf (British Geological Survey; July 2013), Denmark: 0-13.4 Tcf (USGS study; December, 2013), Lithuania***: 36-181 Tcf (Lazauskiene & Zdanaviciute, 2014). This could serve to secure long-term natural gas needs from a domestic source, since currently most European countries rely strongly on imports (Tab.1; only The Netherlands, Denmark and Norway are natural gas exporters).

Tab. 1: Natural gas imports of selected European countries (based on 2009 data, EIA 2011).

| Country | Imports (Exports) | Country | Imports (Exports) | |

|---|---|---|---|---|

| France | 98% | Denmark | (47%) | |

| Germany | 84% | Sweden | 100% | |

| Netherlands | (38%) | Poland | 64% | |

| Norway | (96%) | Turkey | 98% | |

| U.K. | 33% | Ukraine | 54% |

**The U.K. study does not mention a recoverability factor and the shale gas amounts refer only to GIP. A conservative estimate of the TRR would be 82-228 Tcf, or a 10% recoverability factor.

***The Lithuania study does not mention a recoverability factor and the shale gas amounts refer only to GIP. A conservative estimate of the TRR would be 3.6 – 18.1 Tcf, or a 10% recoverability factor.

Positive economic impact

Several reports have concluded that the shale gas industry in the U.S. has created a large number of jobs and has had a profound, positive economic impact, such as reducing consumer costs of natural gas and electricity, stimulating economic growth and increasing federal, state and local tax revenue.

Globally, 32 % of the total estimated natural gas resources are in shale formations (EIA, 2013). Due to its proven quick production in large volumes at a relatively low cost, extraction of shale gas resources has revolutionized the U.S. natural gas industry, providing 40 % of total U.S. natural gas production in 2012 (EIA, 2013).

“The Economic and Employment Contributions of Shale Gas in the United States”, published in December, 2011 by IHS§, concluded that in 2010 shale gas production contributed $18.6 billion in federal, state and local government tax and federal royalty revenues. Also, the study reports the shale gas contribution to GDP to have been more than $76 billion in 2010. An update of the report was published in June, 2012 (“The Economic and Employment Contributions of Unconventional Gas Development in State Economies”) that includes tight gas and coal bed methane as well as shale gas. It is assumed that the unconventional gas industry contributes more than $49 billion annually to government revenues, and will contribute $197 billion to U.S. gross domestic product by 2015. Furthermore, unconventional gas activity supported 1 million jobs in 2010 and this will grow to nearly 1.5 million jobs in 2015.

The study “Ohio’s Natural Gas and Crude Oil Exploration and Production Industry and the Emerging Utica Gas Formation - Economic Impact Study”, published in September, 2011, highlighted the economic contribution and benefits of the natural gas and crude oil industry to the State of Ohio. It included an estimate of the economic impact of planned industry spending on the development of the Utica shale gas formation. One of the findings was that “more than 204,000 jobs will be created or supported by 2015 due to exploration, leasing, drilling and connector pipeline construction for the Utica Shale reserve." A more recent study “America’s New Energy Future: The Unconventional Oil and Gas Revolution and the US Economy. Volume 2 – State Economic Contributions” published in December, 2012 by IHS, reports that the industry paid over $910 million in state and local taxes in Ohio in 2011. Moreover, the IHS study shows Ohio currently has a total of 38,380 jobs related to unconventional gas and oil activity, a number expected to increase to 143,595 in 2020 and to 266,624 by 2035.

§ Information Handling Services (IHS Inc.) serves international clients in five major areas: energy, product lifecycle, environment, security and electronics and media.

Mitigation of climate impacts

Natural gas is the cleanest burning fossil fuel. The climate impact advantage is well established for conventional natural gas, but it has been questioned for shale gas, where increased greenhouse gas emissions during production do occur. Results from recent studies indicate that the impact on climate of shale gas is only slightly higher in comparison with conventional natural gas and significantly lower than coal, when currently available best technologies are used. However, most studies explicitly state large uncertainty in some, or many, of their assumptions, and more research is needed on this topic (see SHIP “Climate Impact”).

What are the risks?

Due to the low permeability of shales, gas production from shales applies hydraulic fracturing of the rocks. A high demand for freshwater, the production of large amounts of waste water, induced seismicity, greenhouse gas emissions, and groundwater contamination have all been linked to hydraulic fracturing technology in the past. Dense well-spacing, noise from operations and increased truck traffic are further concerns for the environment and the public. Economic risks apply to shale gas operators.

The development of technology within shale gas operations has been rapid within the last few years and is still ongoing. Some environmental impacts have already been effectively reduced using these new technological developments. The reduction of greenhouse gas emissions during shale gas production and the reduction of freshwater demands by increased recycling and re-use of wastewater are prominent examples. Other issues still need more attention from research and development, e.g. the prevention of induced seismicity.

Water contamination

Groundwater contamination can happen through spillage via the surface route or by leakage from the wellbore. Leakage of fluids through the rock formations between the targeted shale and shallow freshwater aquifers is in principle also possible, but much less likely.

Wastewater is produced in shale gas operations mainly during the flowback phase, when a portion of the fracturing fluid returns to the surface after hydraulic fracturing. Additional to proppant and chemicals initially present in the fracturing fluid, the returned water will have picked up a variety of elements from contact with the shale rocks, including NORM. This water needs proper treatment for recycling or disposal.

This can be achieved with available technologies, which are currently being developed further to be more efficient and less costly. However, discharge of contaminated waters into rivers, delivery to unsuitable publicly owned treatment works, and spills due to improper surface handling of wastewater have all occurred and need to be investigated, remediated and, importantly, learned from.

Induced seismicity

Hydraulic fracturing causes millions of very small and localized seismic events when the fractures are actually produced in the shale. Recorded by special equipment, operators benefit strongly from this seismic response by pinpointing the spatial and temporal distribution of produced fractures in the underground.

On the other hand, the stress applied to the rocks by hydraulic fracturing interacts with the pre-existing stress field underground and might induce further seismic events that can be larger than the deliberately produced microseismicity. Seismic events apparently connected to shale gas hydraulic fracturing have been documented, and although of small magnitude, have prompted much attention and thorough investigation.

Operational best practices to reduce the risk of induced seismicity have been developed in geothermal energy production, where similar hydraulic fracturing techniques are applied to stimulate flow. These best practices can be applied in much the same way to shale gas production. However, since precise knowledge of the prevailing underground stress field and mechanical properties of the rocks present is always limited, induced seismicity risk-reduction is a complex and challenging task.

Greenhouse gas emissions

Methane, the main component of natural gas, may act as a potent greenhouse gas that contributes to global warming when released into the atmosphere. Large quantities of methane may be released into the atmosphere during the flowback-phase of a shale gas well: when the fracturing fluid is returning to the surface, it brings along natural gas that is released from the freshly-fractured shale.

It was common practice in shale gas developments to release the gas produced during flowback into the atmosphere or to flare it. Flaring (burning) the gas results in the conversion of methane to carbon dioxide, which is also a greenhouse gas. Available technologies, so-called Reduced Emission Completions (REC), can capture the emerging gas at the wellhead. RECs are increasingly applied by shale gas operators for various reasons, one of them being the revenue from selling the captured natural gas.

Water demands

Variable, but large amounts of water are used for hydraulic fracturing. This water may come from natural sources such as rivers or groundwater but increasingly, hydraulic fracturing fluids are recycled and reused. The shale gas industry´s water demands usually make up only a small share of total water usage in a given region. However, this demand must be properly managed in a collaborative effort by industry and regional water planning agencies. In general, the availability of water for shale gas operations should only pose a problem in the world´s arid regions.

Economy

A holistic view of shale gas development must include economic factors alongside the ecological risks and societal issues. The economic risk with shale gas wells is that they require horizontal drilling and hydraulic fracturing, which significantly increases capital costs. Major factors in calculating economic risk and uncertainty include 1) poorly constrained, eventual long-term gas production of shale gas plays, and 2) long-standing and possibly long-term low world market natural gas prices. The economic success of shale gas developments, which has been reported recently, may continue in the future, but is no self-seller.